Bye bye, rye

As ryegrass availability declines and cost increases, superintendents overseed less

The perennial ryegrass market has taken a beating in the past several years. There are two economic factors that have reduced the amount of ryegrass superintendents can use to overseed golf courses — tighter maintenance budgets and crops such as wheat, corn and soybeans that are yielding more profit than grass for growers. Distributors feel the pinch and wonder if the decline of the market has bottomed out and will start to recover.

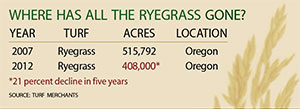

The decline of the perennial ryegrass market started in 2007, about the time growers raised prices. This coincided with the crash of the golf economy, which was followed by the crash of the rest of the U.S. economy. Biofuels were all the rage and displaced significant grass seed acreage.

“Prices started rising at a bad time because superintendents’ budgets were tight,” says Steve Tubbs, president and founder of Turf Merchants, a developer, producer and marketer of turf seed. “Additionally, the price of grass increased after superintendents finalized their budgets, so they ordered less seed and started cutting back on seeding rates and areas that were overseeded or both.”

John Rector, turf products manager for Barenbrug, echoes Tubbs’ sentiment about the declining economy in 2008, when superintendents started to gradually cut back on overseeding because they were constrained by shrinking budgets.

“Superintendents are tied to their budgets when it comes to purchasing seed for overseeding,” says Rector, acknowledging the dramatic fluctuation in the cost of ryegrass the past six years. “These fluctuations make it that much more difficult to accurately budget these costs.”

The bottom line is, economics has changed the way superintendents approach golf course maintenance, overseeding included, says Wayne Horman of Landmark Turf & Native Seed. Perennial ryegrass, for example, is 25 cents more per pound than last year. Distributors paid 71 cents, and now it’s 96 cents.

“If there’s a lot of dead grass this spring, no matter where, we’ll be short on ryegrass,” Horman says. “More acres aren’t being grown, because growers have found more profitable crops — wheat, corn and soybeans, for example — to grow. I don’t think superintendents know how short we can be.”

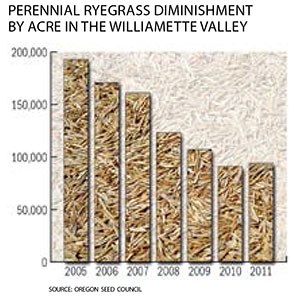

That scenario is the opposite of what happened in 2010, when there was an oversupply of perennial ryegrass, which is grown in Oregon, Washington, Canada and Northern Minnesota.

“New construction was way down, and superintendents’ budgets were very tight, so growers were told the industry didn’t need ryegrass,” Horman says. “As a result, they gradually cut back 25 to 30 percent a year. It was cheaper to plant wheat, corn and soybeans because growers were making more money with those crops.”

Worldwide demand for wheat began to rise about this same time and replaced 40 percent of the cool-season turfgrass production, which was far less profitable. The cost of ryegrass will remain high as long as worldwide demand for wheat outstrips supplies, Tubbs says.

“There are 220,000 acres of wheat that used to be all grass in the Pacific Northwest,” he says. “There has been a steady decline of most cool-season grass acreage since 2008. We lost 25 percent of it that isn’t coming back.”

“Ten years ago, there were a few thousand acres of wheat in Oregon’s Willamette Valley, and in 2012, there were 135,000 acres harvested,” Rector adds.

The profitability and competition from other agriculture products, such as wheat, corn and vegetables, increased options for growers. When seed prices crashed in 2009-2010 and seed acres declined, seed growers looked for options and found rising prices for grain an alternative. However, with increased seed prices, the tide might be shifting again toward grass seed.

“Growers generally like crop rotations and higher-priced seed, and increased demand fits nicely into the mix,” Rector says. “With seed companies back looking for acres and prices favorably competing, we’ll likely seed more acres return to grass seed in the near future.”

Impact

The most significant impact of the economic downturn in the perennial ryegrass market is on overseeding in the South. However, each market, and for that matter, each course, is different. The overseeding market in Palm Springs, Calif., is different than markets in Arizona, which are different than a blue-collar club in North Carolina, where it just might order a cheap seed to keep turf green throughout the winter. Still, less overseeding is occurring in the South because there’s less perennial ryegrass available.

It’s no secret superintendents are a resilient bunch. So, whether it’s because of a tight budget or lack of available seed, they’ll do something different, and golfers will adjust to that. They might be willing not to overseed wall to wall, for example. Furthermore, the new ultradwarf bermudagrasses contribute to the reduction of overseeding greens in the South.

Lower seeding rates persist. About 10 years ago, the average seeding rate was 600 to 800 pounds per acre; now it’s 400 to 600 pounds per acre, Tubbs says. To put seeding rates into a broader perspective, they were at 250 pounds per acre in the 1970s and increased to as high as 800 to 1,000 pounds per acre a couple decades later because the price was so cheap.

“In Palm Springs, there are some superintendents who aren’t overseeding the roughs anymore and are calling it the links look,” Tubbs says wryly. “Five years ago that wouldn’t be the case. Now we’re seeing more acceptance of that.”

That said, Tubbs doesn’t see a drastic difference in playing conditions with the lower seeding rates.

“It all comes back to what golfers want,” Horman says.

Lower seeding rates equate to more coated seed (polymer, water absorbing), all trying to get better results (more seed that survives) with less seed, Horman says.

“The good point of all this is that there’s less turf to mow, water and fertilize. There’s more sustainability. It’s just not good if you’re a seed dealer,” Tubbs says.

In some ways, the ryegrass market has come full circle with perennials and annuals as the industry returns to overseeding with improved turf-type annuals because of the cost of perennials.

“It’s all relative,” Tubbs says.

An eight-year-old Barenbrug project called Turf Annuals validates Tubbs’ point. To provide superintendents with an option to the traditional use of perennial ryegrass for overseeding, the company embarked on a turf project to significantly improve the turf quality of annual ryegrass, which provides some attractive overseeding traits but not the turf quality. Vigorous out of the ground and quick to establish, SOS provides superintendents an option to perennials.

“It can be seeded later in the fall, even with soil temperatures in the low to mid-40s,” Rector says. “It features a naturally smooth spring transition while providing significantly improved turf quality compared to traditional annual ryegrass.”

With seed yields significantly higher than perennial ryegrass, SOS is economical and there’s no need for chemical transition. An alternative for roughs, fairways, driving ranges or other club turf areas, SOS can be mixed with perennials or in stand-alone turf annual blends.

Other less likely alternatives to overseeding with perennial ryegrass include heat-tolerant bluegrass. For example, the Country Club of Birmingham (Ala.) has bluegrass roughs. Poa trivialis has been used to overseed rough, but it’s not as cost effective as rye. It comes down to a balance of aesthetics and agronomics.

“All species of seed will increase in cost, it comes down to finding acres,” Horman says.

A look ahead

While the industry might never see the levels of overseeding that occurred the past decade, the need for permanent turf and overseeded perennial ryegrass has begun to stabilize and improve. And with it will come a need for higher yielding varieties and more acreage.

“As for the new crop of 2013, we’re hoping we don’t see a repeat of 2012,” says Rector, citing the perfect storm of harvest complications last summer that left the seed industry gasping for breath.

A cold wet spring, followed by miserable conditions for pollination, led to a late ryegrass harvest with less-than-optimal yields. The perennial fell over the tall fescue crop, and the two varieties competed for seed cleaning facilities and state seed lab approval. With inventories tight, the inevitable happened, and the industry rolled into fall scrambling for new crop, trucks and trying to make customers happy.

Furthermore, fall 2012 experienced a drought of historical proportions in the Willamette Valley. Newly planted seed fields sat waiting for moisture, and the effectiveness of weed control measures was diminished. And when it rained, it didn’t stop.

“By mid-November it was painfully obvious that what we had was all we were going to get,” Rector says

Tubbs doesn’t foresee the perennial ryegrass market improving any time soon.

“NGF said 154 golf courses closed this past year,” he says. “There are fewer courses, fewer acres. This is not a fad, it’s a trend.”

John Walsh is a freelance writer based in Cleveland, Ohio.

Subscribe to Golfdom

If you enjoyed this article, subscribe to Golfdom to receive more articles just like it.