Appraise an investment before you invest

Part of a turfgrass manager’s role is to propose one or more capital expenditure projects that would benefit the facility. These projects are then proposed to the management board or a greens committee, typically as a part of the budgeting process. The manager and the board probably will have more capital proposals than they have cash to fund them, so a method is required for choosing the most appropriate projects, whether they are machinery, course improvements or clubhouse investment.

Typical capital investment decisions facing the enterprise from time to time include:

Replace or repair/keep? As equipment or facilities become nearly used up, course management must decide whether to repair them and use them longer or replace them. Generally, the older these items are, the more costly the ongoing maintenance.

Purchase capital item A or B? When buying a new machine, the course usually has a choice among different brands, sizes, performance characteristics, etc. While decision-makers may base much of the decision on technical differences, a major consideration has to be the economic differences between competing proposals.

Lease or buy? Golf courses often have the option to buy equipment or lease it, and the course must consider differences in the economics of the two options.

Do it yourself or hire it out? Maintenance and construction work can be done either in-house staff or by outside contractors. Economic differences often are the deciding factor.

These capital investment decisions occur throughout the year rather than as daily operating decisions. Ideally, the manager anticipates these major changes and carefully plans for them.

Appraisal methods

There are several methods of investment appraisal; however, the three main methods are (1) payback, (2) annual return and (3) net present value

Remember when evaluating investment appraisal methods that they all rely on the accuracy of predicted net cash flows over the project lifetime. Net cash flow is the difference between the cash received and cash paid during the defined lifetime period. For example, installation of a drainage system should enable a golf course to be open for more days, bringing in extra revenue. When replacing old machinery, the cash received is the savings on maintenance and repair costs.

We’ll use the three investment appraisal methods by examining three options a golf club has for spending $40,000 available for improvements. The superintendent would like to do one of the following: make course alterations to reduce maintenance time and costs (Project A); upgrade the irrigation system (Project B); or install drainage (Project C). Each of these options is costing the club money through repair bills and loss of income. However, the superintendent can choose only one option because of cash restrictions.

Payback

The payback method estimates how long it will take for a project to start generating an income. It looks at the value of the initial investment compared to the projected net cash flow.

Having calculated the payback period, it may be of interest to calculate the surplus cash generated during the project lifetime after recouping the initial investment. This surplus cash could be from income generated, such as from the purchase of golf carts, or savings on costs, as in replacing old machinery.

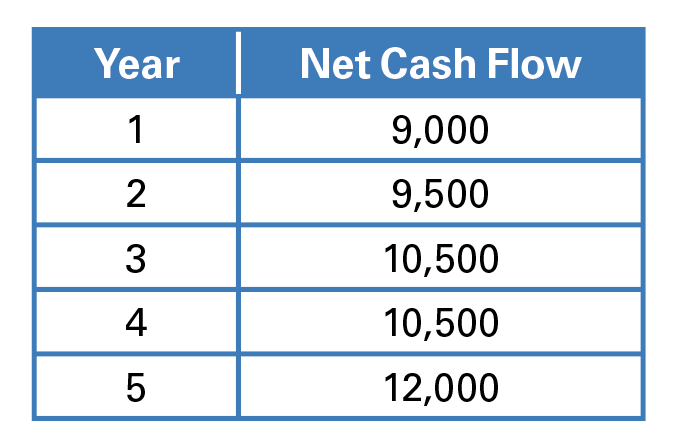

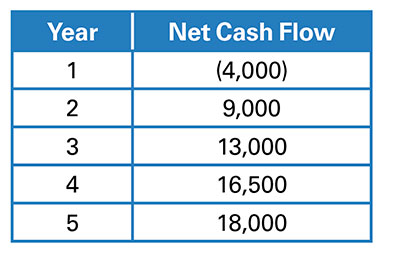

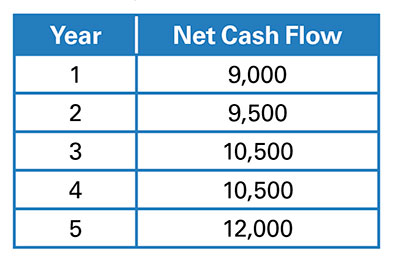

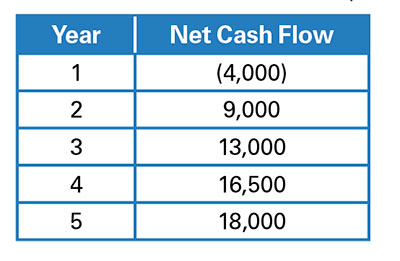

Example 1. Making course alterations to reduce maintenance time and costs</h4.

Calculations from a forecasted maintenance schedule analysis show that if an initial investment of $40,000 is made for Project A, it will generate the following net cash flows (savings in maintenance costs):

Table: Andrew Turnbull

We calculate the above figures by estimating the reduction in maintenance costs compared with keeping the course as it is.

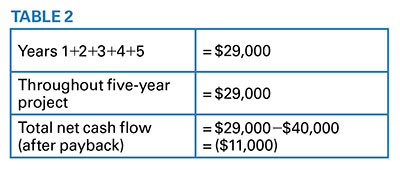

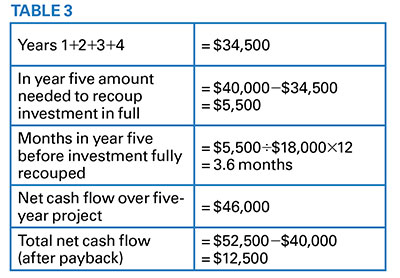

To calculate the payback period of the $40,000 investment, total the net cash flow figures over consecutive years until the full investment is recouped.

Photo: Andrew Turnbull

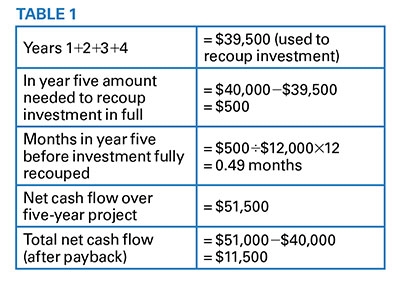

With this example, the investment is fully recouped in just over four years, resulting in a total net cash flow after payback of $11,500 for the five-year project.

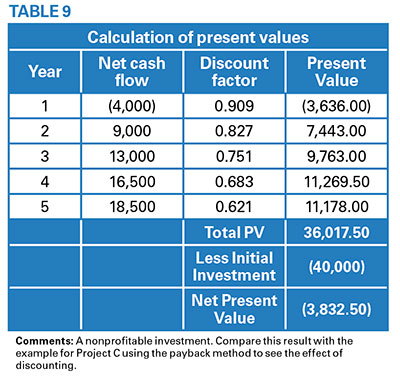

Example 2. Installation of a borehole to replace irrigation water mains

Project B requires an initial investment of $40,000 and is forecasted to yield the following net cash flow figures in water savings:

Table: Andrew Turnbull

Table: Andrew Turnbull

With this project, the initial investment would not be recouped after five years. This does not preclude the project, as ongoing savings may make the project worthwhile.

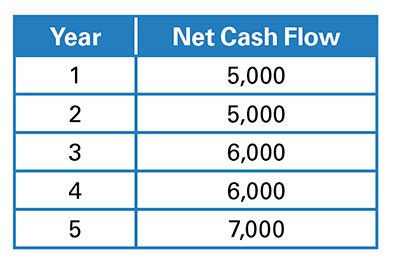

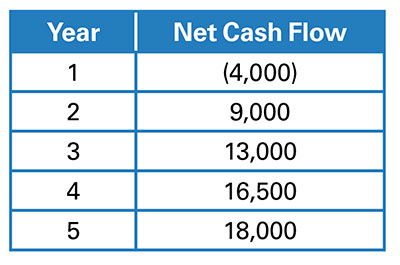

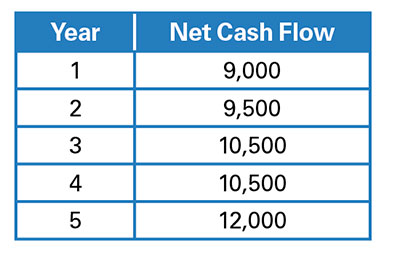

Example 3. Drainage of three fairways that cause regular closure of the course during the winter and loss of green fees

An initial investment of $40,000 into Project C will lead to the following net cash flows:

Table: Andrew Turnbull

Table: Andrew Turnbull

Payback is the most frequently applied technique and is used to screen out projects that take too long to recoup the initial investment. The course would then use a more accurate method of investment appraisal.

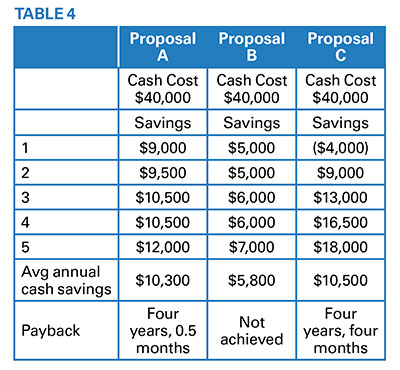

Table 4 shows how to evaluate the above projects using payback as the selection criterion. The cash inflows and outflows for each are shown.

Table: Andrew Turnbull

The payback period can be of some use in screening the three proposals. Proposal A seems to be better than Proposal C; the shorter payback period clearly is better. The course can discard Proposal B outright; its initial cost exceeds future cash savings, so it does not pay for itself. Therefore, with payback, the course accepts Proposal A.

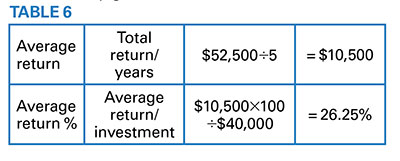

This method has several shortcomings that limit its usefulness. First, the method does not consider the earnings that continue after reaching the payback period. Proposal C, for instance, has a total savings of $52,500 compared to the $51,500 total earnings of Proposal A. The slightly shorter payback of Proposal A may mislead the superintendent who relies solely on the payback approach to evaluating investments. Also, keep in mind that we ignore the time value of money of the cash savings for each proposal when using the payback approach.

Average annual return

Because of unpredictable fluctuations in returns over the life of a project, managers often use average return as a slightly more accurate measure of investment appraisal.

It averages total return (net cash flow) over the duration of the project.

The average annual return can also be converted into a percentage in relation to the value of the initial investment.

Course managers may use both these figures as a basis of comparison for different investment proposals. Initially compare the average annual return percentage with the business’s cost of capital (explained in discounted factor, next page).

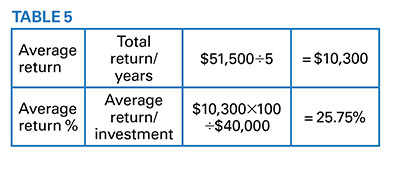

Example 1

Using the figures for Project A, which had an initial investment of $40,000:

Table: Andrew Turnbull

Table: Andrew Turnbull

Example 2

Using the figures for Project C with an initial investment of $40,000:

Table: Andrew Turnbull

Table: Andrew Turnbull

Net present value

Both payback and average return have a major drawback in that they ignore the “time factor” that $1 received today is worth more than $1 received in one year’s time.

The net present value is the net value of the future cash flows. Said another way, the value of the future total cash value flow minus the initial capital investment.

The cost of capital is the sacrifice made by the business by investing in a project. This considers:

- Comparison with returns from investing the capital in an alternative way, such as an account in a bank;

- Interest on debts incurred to raise the funds to finance the project;

- The time value of money.

Table: Andrew Turnbull

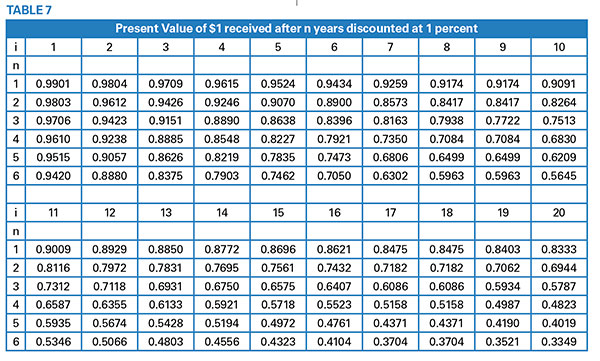

Discount factor

We use discount factors to calculate the present value of predicted net cash flows. Table 7 shows a discount factor table, used to provide the relevant discount factor for specific rates of costs of capital.

The discount factor used for a net cash flow after five years at a cost of capital of 6 percent would be 0.7473. Therefore, a predicted net cash flow of $100 in five years’ time at 6 percent would have a present value of $100 x 0.7473 = $74.73.

Example

(1)Apply the 10-percent discount factor to the following Project A figures to calculate the present value of the future cash flows.

(2) Calculate the net present value of the project where the initial investment is $40,000.

Table: Andrew Turnbull

Table: Andrew Turnbull

Table: Andrew Turnbull

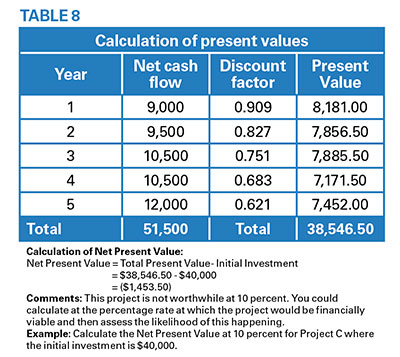

Example

Calculate the net present value at 10 percent for Project C where the initial investment is $40,000.

Table: Andrew Turnbull

This shows a nonprofitable investment. Compare this result with the example for Project C using the payback method to see the effect of discounting.

Considering cash flow

Capital budgeting focuses on the acquisition of facilities and equipment. The methods presented here consider the cash flows related to the proposed project. First, there is the initial cash outflow, which is the cost of the investment. Second, there may be cash inflows and cash outflows or cash savings over the life of the investment.

The payback approach determines the number of years required for a project to pay for itself. This approach is best used for screening projects for further consideration using the net present value approach.

The net present value approach considers both the amount of the cash flows and the timing of the cash flows. Using present value factors, future cash flows are discounted to the present time and compared with the initial cost of the project.

When considering a single proposal, if the net present value of a proposed investment is equal to zero or is positive, make the investment.

Andrew Turnbull BSC (Hons), Dip. RSA, Cert Ed., is the owner of AllTurf Management and managing director of the Great Lawn Company Ltd. Contact him at allturfman@ntworld.com. This article was previously featured in Pitchcare and is reprinted with their permission.

Subscribe to Golfdom

If you enjoyed this article, subscribe to Golfdom to receive more articles just like it.